To calculate used car depreciation, apply the declining balance method by multiplying the vehicle's current book value by its annual depreciation rate (typically 15–25%) and repeat year by year to project value loss. Then adjust for mileage, condition grade, and title history to arrive at Actual Cash Value (ACV) — the number that tells you what the car is actually worth and sets the ceiling for any negotiation.

What Car Depreciation and Value Loss Mean for a Used Car Buyer

Car depreciation is the loss in a vehicle’s value as it ages, is driven, and changes hands. For a buyer, the goal is not to stop value loss. Try to avoid buying after hidden damage has already occurred. The sharpest drop often comes when buying a new car. Many models can lose value more quickly than expected. The loss also affects financing, trade-in power, and insurance payouts. When you buy a car, new or used, you are buying transportation and future resale value.

Use these signals:

- Compare the asking price with similar listings in your region.

- Check whether the vehicle has already absorbed first-year depreciation.

- Ask an essential question: How much does a car depreciate for this model, not just for the segment?

- Review maintenance records, accident history, title brands, and mileage.

- Create a small depreciation chart so you can see whether the car’s value drops look normal.

- Include the drop in total cost of ownership, not only fuel and repairs.

What Is Actual Cash Value and How Is It Calculated?

Actual cash value, or ACV, is the insurer-style estimate of what a vehicle is worth right before a loss. The National Association of Insurance Commissioners (NAIC) states that ACV coverage pays based on the value after accounting for age and wear and tear. A vehicle history report gives you the facts needed to challenge a weak number. It can show whether a clean-looking vehicle should be priced below clean retail.

How to calculate ACV:

- Start with three comparable retail listings for the same year, trim, engine, and area.

- Remove outliers, then use the remaining prices to estimate a fair price.

- Subtract visible repair needs, worn tires, overdue service, and missing keys.

- Subtract title penalties, prior theft, flood notes, or branded records.

- Adjust for mileage by comparing the odometer with normal use for that model year.

- Use this result as the car's fair market value before taxes, fees, warranties, or add-ons.

- Compare that car's depreciated value with the car insurance settlement logic if the vehicle was recently damaged in an accident.

- Record the final depreciated value. Keep the worksheet.

How to Choose the Right Depreciation Formula for a Used Car

Choose the formula that matches your goal. Use straight-line for simple planning, declining balance for early drops, and odometer-based math when use is unusually high. A car depreciation calculator can help. However, your own notes reveal why depreciation starts and how to find depreciation rates. You can also combine methods to improve accuracy. For example, use straight-line depreciation to estimate long-term ownership costs, then compare the result with real market listings to see whether the vehicle is losing value faster or slower than expected.

Straight-Line Depreciation

The straight-line depreciation method spreads the expected loss evenly across the ownership period. The Internal Revenue Service (IRS Publication 946) says the straight line applies a depreciation rate to the adjusted basis and uses the required convention in the first and final year. That tax rule is not the same as retail pricing, but the logic is useful. It works best when you plan to keep your car for a known period. It also makes the length of car ownership easy to compare across options. Use it when you want a clean planning estimate, not a perfect resale forecast.

Apply this simple car depreciation formula:

- Estimate what the vehicle will be worth at the end of your ownership period.

- Subtract that residual value from today’s price.

- Divide the difference by the years owned.

- Example: $24,000 today - $15,000 later = $9,000.

- Over three years, that equals $3,000 per year.

- This gives the average car depreciation per year for your budget.

Declining Balance Method

Declining balance assumes the vehicle will depreciate faster early and slower later. IRS Publication 946 describes it as using the same rate on an adjusted basis each year when that method yields a higher deduction.

It explains why a new vehicle can lose much value early. Shoppers buy a new car only when incentives offset that loss.

Mileage-Based Depreciation

This method focuses on usage rather than age. It is helpful when driving your vehicle far above or below normal. A low-mile commuter may maintain its value better than an identical high-mile example. A delivery vehicle can depreciate faster, even with clean paint. Odometer patterns also help assess vehicle depreciation when service records are incomplete.

Use this approach when the odometer is the primary factor:

- Find the expected annual mileage for a vehicle of that age.

- Compare it with the actual odometer.

- Compare prices with similar listings with higher and lower odometer readings.

- Estimate a depreciation adjustment from those comparable listings.

- Apply additional depreciation for severe use, rideshare, towing, or commercial duty.

- Reduce the penalty if records show timely service and quality repairs.

Hidden Value Killers That Silently Reduce ACV

Some problems reduce ACV before a buyer notices them. Title brands, open recalls, poor repairs, odors, missing emissions equipment, and weak service history all matter. The biggest danger is paying full market price for a vehicle that cannot prove a clean story. Many hidden value losses appear only during resale, financing, or insurance evaluation. Inconsistent maintenance intervals, aftermarket electrical work, corrosion under the chassis, prior airbag deployment, water intrusion, and incomplete ownership records can all lower buyer confidence.

Salvage Title and Total Loss Threshold

A salvage title means an insurer or authority found the damage serious enough to brand the record. The exact total loss threshold depends on state rules and insurer math. Vingurus is a service that helps replace guessing with title events, ownership clues, auction notes, and damage records. Use the VIN decoder first. Decide whether the deal still deserves your time. The lower price must be large enough to match the risk.

Watch for these red flags:

- Salvage, rebuilt, flood, junk, lemon, or export title notes.

- Auction photos that show hard hits before repairs.

- Repairs close to or above the value of the vehicle.

- Airbag deployment, structural notes, or missing safety labels.

- Seller language like “minor issue” with no repair invoice.

- A price that is low but not low enough for the risk.

Odometer Rollback

An odometer rollback makes a vehicle look newer than it is. Any drop or strange gap should lower trust, even if the dashboard looks normal. Mileage inconsistencies can affect financing approvals, warranty eligibility, insurance valuations, and future resale negotiations. Buyers should compare odometer readings with service invoices, inspection reports, emissions records, and historical registration data.

Condition Grade and Frame Damage

Condition grade changes what the make and model of a car can command in the real market. Two identical trims can price thousands apart if one has poor paint, weak brakes, interior abuse, or structural damage. Before an appraisal, assess the vehicle honestly. This will help you calculate car depreciation and protect the vehicle's value before paying for an inspection. The goal is to decide whether the inspection is worth booking.

Use this inspection checklist first:

- Exterior (paint match, rust, dents).

- Interior (seat wear, odor, stains, electronics).

- Tires and brakes (tread depth, rotor condition, uneven wear).

- Mechanical (leaks, noises, warning lights).

- Structure (weld marks, bent rails).

- Records (service dates, owner history, recalls).

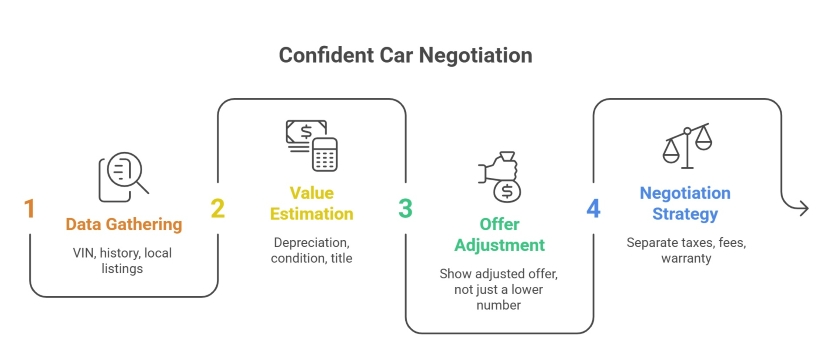

How to Use Your Depreciation Calculation to Negotiate a Lower Price

A seller may defend the sticker price. Nonetheless, numbers help structure the negotiation. Bring comparable listings, your ACV estimate, and a written adjustment sheet. In this case, Vingurus helps because documented history gives you proof, not opinion. If the report shows issues, you can explain the car's resale value with confidence.

Follow these steps:

- Confirm the VIN, trim, and mileage readings.

- Pull the vehicle history data and note any risk that affects car values.

- Compare three local listings and remove unrealistic outliers.

- Estimate actual depreciation from age, use, title, and condition.

- Show your adjusted offer, not just a lower number.

- Separate taxes, fees, warranty products, and trade-in discussion.

- Leave room to walk away if the risk is evident.

- Save your worksheet for lender, insurer, or appraiser questions.

How Car Depreciation Affects Your Loan and Equity Position

Value loss can outpace your loan balance. Compare your depreciation schedule with the loan’s amortization schedule before signing. A small down payment, long term, and high interest rate can leave you upside down. Negative equity becomes a larger risk when vehicles depreciate quickly during the first years of ownership. Rolling old debt into a new loan, paying dealer markups above market value, or financing taxes and add-ons can widen the gap between what the car is worth and what is still owed.

Which Used Cars Lose the Least Value?

The lowest depreciation usually appears where ownership costs are predictable. Demand stays strong, and supply is limited. A low depreciation rate can also preserve your car's value when you resell it. Trucks, hybrids, practical compact models, and some enthusiast models often hold their value better than high-priced luxury or fast-changing EV models. Still, pricing is local. When car shopping, compare segment trends with the specific condition of the used vehicle in front of you. The value of the vehicle depends on proof, and average depreciation should never replace inspection.

|

Vehicle Category |

Average 5-Year Residual Value (%) |

Depreciation Risk Level |

Best Buyer Profile |

|

Midsize trucks |

65.8 |

Low |

Drivers who tow, haul, or want durable utility |

|

Hybrids |

64.6 |

Low |

High-mile commuters who want fuel savings |

|

Small SUVs |

58.3 |

Medium |

Families who need daily practicality |

|

Overall market |

58.2 |

Medium |

Buyers comparing many body styles |

|

EVs |

42.8 |

High |

Tech buyers with home charging and discount focus |

|

Large luxury SUVs |

47.9 |

High |

Buyers who value comfort over resale protection |

Key Takeaways

- Car depreciation is the rate at which a vehicle loses its value over time.

- To calculate vehicle depreciation, compare prices, condition, title history, and odometer records.

- A car will depreciate differently by brand, trim, demand, usage, and repair quality.

- Start by using a car depreciation calculator for a quick range. Then, verify with records.

- Maintain your car, document repairs, avoid poor modifications, and fix small issues early.

- The impact of depreciation varies; it is largest when the loan payoff stays above what the car is worth.

A careful buyer needs clean records and the discipline to adjust the offer. If the car has depreciated more than the seller admits, this is a red flag. Good data makes the discount defensible.

Frequently Asked Questions

Why Does Depreciation Slow Down After the First Few Years?

Buyers pay premiums for freshness, warranty, and low uncertainty. This causes faster depreciation. A new car can lose significant value in the first few years. Then, the decrease in value gets smaller.

Does Depreciation Pause If a Car Is Stored and Not Driven for a Year?

No. Storage can slow depreciation tied to use. However, age, fluids, tires, batteries, market shifts, and demand still reduce how much value your vehicle retains.

How Do Trim Levels Affect Depreciation Differently Within the Same Model?

A car is valued more with a popular trim with useful features. A rare luxury package may not retain its value.

Can I Deduct Car Depreciation If I Use the Vehicle for Business?

Maybe. Car depreciation for tax purposes depends on how you use a car. Consider whether the vehicle is used for business and what records are available. Ask a tax professional about any tax deduction.

Does CPO Certification Actually Slow a Car's Depreciation Rate?

CPO can minimize depreciation when buyers trust the inspection and warranty. It does not erase age, use, accident history, or weak demand. Nonetheless, it can support a stronger price.