To check if a car has a lien before you buy it, verify the VIN through the state DMV title database, inspect the physical title, review a vehicle history report, and confirm any listed lender directly. A lien means a bank, lender, or creditor may still have legal rights to the vehicle, even after it is sold. The safest purchase is possible only after the lien is officially released or the lender is paid using verified payoff instructions.

What Is a Vehicle Lien — and Why Does It Follow the Car

A lien means someone else has a secured interest in the car until a debt is settled. A lien is a legal claim against the property, which serves as collateral. The owner of the vehicle may drive it, insure it, and list it for sale. Still, the creditor can stop the transfer or repossess the vehicle if the debt is not handled. That is why the lien on the vehicle follows the title.

This can happen through several common situations:

- The car loan was not fully paid.

- A title loan or title pawn was taken against the car.

- A shop decided to file a mechanic’s lien after unpaid repairs.

- A tax agency chose to file a tax lien.

- A court judgment is attached to the car’s title.

Active Lien vs. Lien on Record

Not every reported claim means money is still owed. An active lien usually points to an unpaid balance or an unresolved lien holder. A lien on record can also show that the loan has been paid, but the release has not been processed by the state. That difference matters because a buyer needs proof, not a promise.

|

Status |

What It Usually Means |

Buyer Risk |

What to Ask for |

|

Active |

The debt may still exist |

High |

Current payoff letter |

|

On record only |

Paid but not cleared |

Medium |

Original lien release |

|

No record |

No listed claim |

Lower |

Matching seller ID and title |

Voluntary vs. Involuntary Liens

A voluntary car lien usually starts when the borrower signs financing papers. An involuntary claim appears because someone says they are owed money. Both can prevent a clean title transfer. The key is knowing who placed it and why.

|

Lien Type |

Who Places It |

Why It Happens |

How Common It Is |

|

Auto loan lien |

Bank |

Unpaid loan |

Very common |

|

Mechanic’s lien |

Repair shop |

Unpaid repairs |

Occasional |

|

Tax lien |

Tax agency |

Unpaid taxes |

Less common |

|

Judgment lien |

Court |

Lawsuit judgment |

Less common |

How to Check if a Car Has a Lien on It

If you are wondering how to check whether a vehicle has a lien, start with the VIN, the seller’s ID, and the current title. Compare state records, vehicle history reports, and lender paperwork. A reported lien does not always mean the debt is still outstanding, but you should never pay for a vehicle until the lien status is verified through the DMV or the lender directly. The safest transaction happens when the lender confirms the payoff amount.

State DMV Title Status Search

Most states let buyers or owners review record details through the official channels, although access and fees vary. A state’s Department of Motor Vehicles (DMV) may show whether the record shows an open claim, whether a transfer is pending, or whether the seller requested a lost car title.

Use the local DMV record first. A lien search matters because the state record controls registration and plates, as well as the procedure of transferring the title.

The New York DMV states that it can take up to 45 days to receive a title certificate by mail.

Getting a Vehicle History Report

A paid report is not a substitute for state records, but it helps a used car shopper spot issues early. Consider VINGurus a platform that makes this easier because you can search by VIN and review accident, ownership, theft, and lien information in one place. If you want to know how to find a lien on a car before meeting the seller, this is a practical first screen.

A good vehicle history report may show:

- A title has a lien or has had one recently.

- A title lien reported by a prior data source.

- Brand, salvage, theft, or odometer records.

- Registration gaps that need explanation.

- Clues that point to title fraud.

Reading the Physical Title

The physical document remains important with digital records. Match the VIN on the dashboard to the number on the paperwork. Review the owner's name, signatures, dates, and lien section. The vehicle’s title should also match the car title and registration details. If not, proceed with caution.

Before you pay, look for:

- A lender is listed on the title.

- A stamped or signed lien release document.

- An original paper title, not a blurry photo.

- Corrections, erasures, or missing pages.

- A note showing the car title is lien-free.

Calling the Lienholder Directly

Call the lender with the seller present or with written permission. Ask whether there’s a lien, what the outstanding loan balance is, and how payment must be made. Do not rely on a screenshot as proof. To verify the lien, contact the lender's payoff department, not a random number in a marketplace message.

The Financial Math — How a Lien Changes What You Should Pay

A lien changes the deal because the seller does not receive the full payment. Part of your payment must satisfy the balance first. If the asking price is $18,000 and the payoff is $12,000, only $6,000 should go to the seller. That is why buyers should focus on the seller’s actual equity, not just the advertised price. A verified payoff amount also helps you calculate whether the discount is large enough to justify the added paperwork, waiting time, and title-transfer risk involved in a lien transaction.

What Is a Payoff Quote and Why Does It Control the Deal

A payoff quote is the amount required to close the account by a specific date. It is different from the monthly balance shown in an app because interest can accrue daily. It also tells you how to know if a car is paid off. Without it, nobody can safely calculate the seller’s equity.

The quote should show:

- Borrower name and account reference.

- Good-through date.

- Per-day interest after that date.

- Exact wire, bank draft, or online payment instructions.

- Where final documents will be sent.

How to Structure a Safe Closing When a Lien Is Involved

A safe closing makes the payoff traceable. Do not hand the full amount to the seller and hope the debt gets cleared. Use the lender instructions, keep receipts, and consider escrow at closing for larger purchases. VINGurus can support this step by helping confirm the vehicle’s lien status before you set the appointment.

Follow this order:

- Run a VINGurus report and a VIN decoder result using the vehicle identification number.

- Get the fresh payoff letter directly from the lender.

- Pay the lender first, then pay the seller’s equity.

- Confirm where you will receive the title and release.

- Submit paperwork to the DMV for lien removal and an updated title.

How Long Does It Take to Remove a Lien From a Car Title?

Timing depends on the state, the lender, and whether the record is electronic. In electronic lien and title states, digital records can clear faster. With a paper process, you may need to receive the lien release document, visit the state office, and wait for a new title. In many electronic-title states, the lien release appears in the DMV system within 3–10 business days after payoff. Paper title states can take 2–6 weeks because the lender must mail the release and the DMV must issue an updated title.

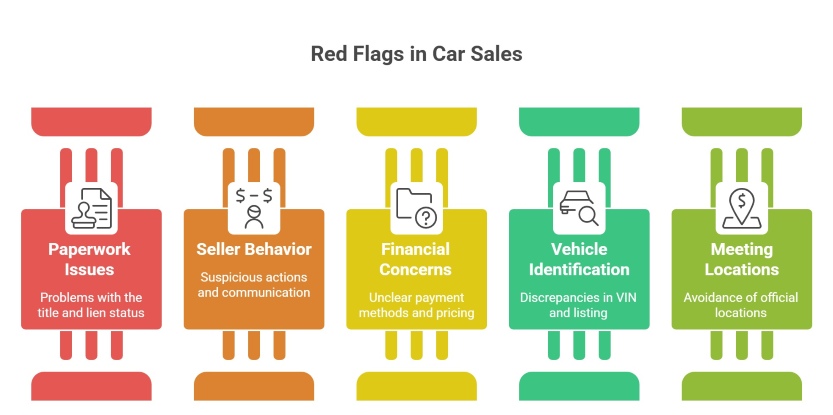

Red Flags — Signs a Seller May Be Hiding a Lien

A seller who is transparent will not rush the paperwork. Pressure, vague answers, and changing stories are warning signs. Some sellers confuse a title loan with normal financing, while others know the title is not ready. Your auto credit score is not the issue here; ownership risk is.

Use this red-flag checklist to check your car’s paperwork and tell if a car needs more review before you agree to buy a vehicle:

- The seller cannot explain why the lien title is still open or why a lien on the car remains.

- The name on the title does not match the seller.

- The seller says the title is free, but shows no proof.

- The seller wants cash before the bank is paid.

- The seller mentions selling the car but avoids payoff details.

- The seller says they will sell a car now and mail the paperwork later.

- Only a photo of the title is available.

- The car seems underpriced for no clear reason.

- The VIN on the car does not match the listing.

- The seller avoids meeting at the bank or DMV.

- The seller claims the lender is closed or unreachable.

The Federal Trade Commission (FTC) reported more than 100,000 complaints in each of four years about motor vehicle sales, financing, service, warranties, rentals, and leasing.

What to Do If You Find a Lien After the Sale

Finding a lien on your car after payment is stressful. Keep every message, receipt, report, and bill of sale. Contact the seller, the lender, and the DMV in writing. If the seller misrepresented ownership, talk to an attorney or consumer protection office.

|

Possible Outcome |

Who Controls the Outcome |

Can the Buyer Fix It? |

Best Immediate Action |

|

Repossession |

Lender |

Sometimes |

Pay, dispute, or seek legal help |

|

Registration denial |

DMV |

Sometimes |

Bring proof and ask what is missing |

|

Legal dispute |

Court |

Sometimes |

Preserve documents and get advice |

|

Delayed title |

Seller |

Yes |

Demand signed release and transfer papers |

VINGurus is useful after a surprise problem because it gives you a clearer record timeline. A lien check can show whether liens on your vehicle appear in data sources. It may help you explain the issue to a lender, insurer, or buyer.

The U.S. Department of Justice reported a federal fraud case involving a scheme to strip liens from 100 cars.

Key Takeaways

- A vehicle lien travels with the car's VIN, not the seller. It survives the sale until formally discharged in the DMV record.

- A clean title only protects you when the VIN, seller ID, DMV record, and lien release document all match.

- A reported lien on a vehicle history report is not proof of an active lien. Always verify the current title status directly with the state DMV before agreeing to any price.

- If a lien is disclosed, the safe offer price equals market value minus the lien payoff amount, not the full asking price.

- The safest closing structure pays the lienholder directly first. Never hand the full amount to a seller and trust them to clear the debt afterward.

- An electronic lien release can take 1–30 days, depending on the lender and state. Confirm the DMV record is updated before attempting to register the car in your name.

- If you discover an active lien after purchase, contact the lienholder in writing immediately. Repossession can happen without prior warning, even months after the sale closes.

Checking first is cheaper than fighting later, especially when you are buying from a private seller.

Frequently Asked Questions

Can Multiple Liens Exist on the Same Car?

Yes. More than one creditor can claim the same car. Priority depends on state law and when each claim was recorded.

Can Unpaid Parking Tickets Create a Lien on a Vehicle?

Sometimes. Some cities can place holds or debts against registration. Certain unpaid government debts may become a claim. Rules vary by state and local law.

Is Refinancing a Car the Same as Removing a Lien?

No. Refinancing usually replaces one lender with another. The old claim may be released. Nevertheless, the new lender records its own interest until the refinanced debt is settled.

Can a Bank Repossess a Car I Already Bought from Someone Else?

Yes, if the prior debt remains secured and the paperwork has not been cleared. A buyer may have claims against the seller. However, the bank can still act.

Can I Register a Car Before the Lien Is Removed?

Sometimes. Some states allow registration with a recorded claim. Others may block the transfer until the paperwork is complete. Ask the DMV before paying the seller.